Practice accounting entries I would approach this practical cases solved by the technique of double-highlighting in each year accounting for a particular operation in order to leave on a good foundation (hopefully).

Note: account numbers used here are those of the Belgian accounting are not the same as the French accounting plan. But what is important is that the accounting logic is the same everywhere and that is what this blog is trying to clarify. objectives of these exercises: We try these exercises to clarify the maximum entries to pass due to practical examples of trade that I will treat each individual operation in contrast to what is found in the usual accounting exercises, where we are faced with a multitude of data, which is, in my opinion , confusing and does not have much of a learning perspective.

So, focusing on specific cases we parvienderons to have an overview and understand the logic on which accounting transactions are established.

I said one important thing about these exercises is that the main purpose is not to learn how to save operations in the various accounting records (journals, balance sheet, income statement ...) for the simple reason that it is only for administrative tasks and complete these documents you need a ruler, a logic, a technique is that of double-and that's why we try to highlight the main objective to be achieved via this blog.

Some important reminders

Before starting these exercises, it is important to understand these general rules are the foundation of any accounting entry:

- Note that assets balance sheet represents the assets while liabilities represents debts

- debts and assets are classified according to accounts by well-defined chart of accounts and each account there are two parties namely the flow and credit

- An account of active increases its speed and an account of liabilities increased its credit and vice versa. [ as an example the purchase of a machine increases the assets, to illustrate this increase is increased the flow of machine account (asset account) and on the other hand, the increase in debt to the supplier is illustrated by the increase in account payable to his credit (liability account). ] For an account

- well defined, if throughput is increased while the credit of the account represents a decrease. [ example, payment of a supplier is reduce the debt that will be illustrated thus debiting the account provider, whereas in the previous example has been credited to increase the debt to the supplier ]

Debit balance :

is the positive difference between total flow and total credit the same account. active accounts still show a debit balance with the exception of bank account that could present a credit balance (rarely).

Credit Balance:

is the positive difference between total credit and total debit of one account. The liability accounts have credit balances. See also

to get used to the concepts of debit and credit and learn to read a balance sheet

Do worry if you do not find these rules quite clear. In all matters, what is harder to learn what the rules are. But, cons, which is easy to understand is the practice rules for it by doing that we could grasp the meaning and operation of things.

Exercises 1. start with the more typical examples that may be encountered in practice. Often asked in job interviews.

You are responsible for general accounting, purchasing goods from Euro 1000 with a 6% VAT. How are you proceed in your accounts?

The first thing to do is determine which accounts will be affected by this commercial transaction. Oops I forgot one little rule. Well do not panic, here it is:

- accounts Class 6 (accounts which represent expenses) increase in throughput and decrease the credit just like the asset accounts, while accounts of Class 7 ( products) follow the same direction of change that the accounts of liabilities, ie increase and decrease in credit flow.

In the exercise, accounts that will be changed are: Purchases of goods

,

Suppliers (

If you buy then automatically there is this account to vary) and VAT. But which one? VAT payable or VAT to be recovered?

Since we buy, we will pay VAT to the supplier

( who will take care of VAT payable to State ) but we will charge (recovery) for sale to the customer which, as a final consumer pays the tax indirectly to the state. Well, I do not know if it's clear explanation, but as you will understand more clearly

on this blog dedicated to VAT .

So is the account of VAT to be recovered

need for change, which gives us the recording below:

D: Flow;

C: Credit

Suppose we we don ' have performed this operation throughout the year. What would happen there at the income statement and balance sheet at the end?

Income statements are accounts of income and expenses. To calculate the benefit expense is deducted from the amount of products. In the above example we have:

Products - load = 0 (no sales) - 1000 (buy) = - 1000 EUR which means a loss of EUR 1000. This loss is reported in the Final count:

For information in the column balance sheet, it displays the accounts receivable balances of assets and liabilities in the column, we put the credit balances in liability accounts. For more details, click

how to read a balance sheet .

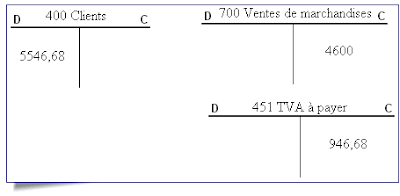

2. We send an invoice to Mr X:

Sale of Goods 4500 EUR;

Transport 100 EUR;

2% discount if paid within eight days, 21% VAT

Before answering, we must clarify the concept discount:

discount is a reduction in price of the merchandise if paid within the period mentioned in the invoice.

- Discount = (4500 +100) x 2% = 92 EUR

It is not included in the taxable base (=

amount is calculated based on which VAT ).

- Taxable base = (4500 +100) - 92 = 4508 EUR

- VAT = 4508 x 21% = € 946.68 this amount is credited to the account level VAT payable ( We'll pay the State instead of the client ). It is a liability account so it increases if the credits.

It is not deducted from Total liabilities at the invoice.

Transport is recognized as a commodity so we have in this case 4600 to be credited to the account level

Merchandise Sales (

remember! This account is a product so it increases the crediting ).

course every sale there is the customer account that will increase in throughput because it is an active account. This increase equals the price of the goods (4600) plus the amount of VAT (946.68), ie € 5,546.68.

End result:

3. We have a lack of liquidity in our case and we decided on April 3 to pour 500 EUR drawn on our bank account using a check (No. 32).

3. We have a lack of liquidity in our case and we decided on April 3 to pour 500 EUR drawn on our bank account using a check (No. 32).

April 05, we receive a debit advice (No. 3) of the bank for payment of the check (No. 32).

How to save this transaction level accounting?

First, it is important to note here that the recording of transactions made on the basis of vouchers and upon their receipt. In this case we have two operations to convey.

- The first is April 03 at the time of issuing the check for an internal transfer of funds. This operation involves two active accounts as follows: The account "cash" account and the "internal transfer". As a reminder, an active account increases throughput and reduces the credit. Consequently, our fund will increase the flow of funds account and the account will reduce internal transfers to credit as a result:

- The second is dated April 05, when receiving the debit of the bank justifies good reception of EUR 500. In this operation, we have reduced the account "bank" credit (asset account) and is increased, in part against the account "internal transfers" to the flow as shown below:

4. A supplier sends us an invoice for:

the purchase of goods: 800 EUR

Packaging: 300 EUR 200 EUR which included

VAT 21% What is new in this example, what are the packages that can be classified into two categories: Those

- definitely be bought without making them later to the supplier. This kind of packaging we recognize it as a commodity. What makes our case, an amount from 900 EUR merchandise to debit . Are considered part of the same class packaging waste.

- And those we need to make to the supplier, this type of packaging is recognized separately under the account " 4166 Packaging equipment and make . It is an active account so we will increase the flow of EUR 200 . Note that this amount is not subject to VAT therefore not included in the tax base.

The amount of the deductible VAT to charge

: (800 + 100) x 21% = 189 EUR

The total amounts to charge is recorded, in part cons,

credit account "Suppliers", ie an amount of (189 + 200 + 900) = 1289 EUR

5. We bought a cabinet that we have to amortize at a rate of 150 Euro to depreciation expense each year for 5 years. Which transaction record at the end of the first year?

5. We bought a cabinet that we have to amortize at a rate of 150 Euro to depreciation expense each year for 5 years. Which transaction record at the end of the first year? The depreciation expense is the estimated proportion of the wear of the cabinet during the year, so it is a burden borne by the company. To illustrate this increase in costs we will debit the account "630 staffing amortization. "cons in part, it decreases the value of the cabinet recorded as assets under the account" furniture and office equipment ", by debiting the" 24,090 Depreciation on furniture, "which gives us the following scheme:

Learn more by visiting

methods of calculating depreciation and accounting treatment. ---------------------- ---------------------------------

For the next exercises we'll move on to another form of writing more simplified but retains the same logic that writes "T". We will use the journal entries.

To learn more about the accounting document (journal) is a mandatory document that is used to record daily, in chronological order, recording all the transactions of the company.

The shape of the log book:

information that interests us here is what is in the middle of the table are:

Account name to be debited to

Title of account to be credited

For application, we write some previous operations in the form of writing Book log:

1.

In the journal we write

VAT recoverable 411 60 604 Purchases of goods

1000 to 440 in 1060

Suppliers

2.

5546.68

400 customers to 451 946.68 VAT payable

700 Sale of Goods 4600

I hope these two examples are sufficient to understand the transition from writing to another.

-------------------------------------------------- -------

6. A customer buys goods from a supplier on January 1 for an amount of 2460 Euro. The buyer received a letter of exchange for agreement to sign and return to the supplier. At maturity (25 January), the provider takes the bill of exchange. The bill is a commercial document which allows the supplier (also called the shooter) to give orders to its client (the drawee) to pay a specified amount to a designated person (the supplier) and a deadline.

In writing amount of a bill of exchange transaction, we use the two accounts "notes payable" and "Accounts receivable" as illustrated below:

Accounting for the bill in the accounting of customer :

January 1 :

604 Purchases of goods

2460 440 2460 Suppliers

January 25 :

440 2460 Suppliers

441 Notes payable 2,460

Accounting for Bills of Exchange in the supplier's accounts :

January 1 :

400 customers in 2460 to 704

merchandise sales in 2460

January 25 :

401 Notes receivable 2,460 400 reviews

2460

7. We receive an electricity bill for $ 250 Euro (VAT 21%). 4111 VAT. 52.5 deductible

61,202 Services and other goods - Electricity 250 to 440

Suppliers 302.5

continued ...

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}